-

6 min read

Nov 3, 2025 9:03:17 AM

Share On:

As an advisor, you’ve likely seen the headlines about a possible U.S. manufacturing revival. While the data shows a mixed picture, certain sectors are experiencing real momentum—momentum that could translate into compelling opportunities in industrial real estate.

Manufacturing’s Uneven but Undeniable Signs of Resurgence

Manufacturing still accounts for roughly 9.7% of U.S. GDP, and as of June 2025, output posted a 0.8% year-over-year increase. These are modest numbers, but they mask the strength of select subsectors benefitting from policy incentives, reshoring trends, and rising demand in high-value industries.

Several policy measures are contributing to this resilience. The CHIPS and Science Act is directing more than $52 billion toward semiconductor research, development, and manufacturing. The Inflation Reduction Act allocates hundreds of billions toward clean energy initiatives, while the Infrastructure Investment and Jobs Act is funneling over $1 trillion into transportation, utilities, and broadband upgrades.

Reshoring is another tailwind. After years of offshoring, manufacturers are re-evaluating supply chains to reduce reliance on overseas production. However, this trend is highly sector- and location-specific—benefiting regions with the right workforce, infrastructure, and policy incentives.

That being said, the broader picture remains complex. The ISM Manufacturing PMI has remained under 50 for several months, signaling overall contraction. Yet even in this environment, high-demand verticals are outperforming the broader index.

Sectors at the Center of Growth

Several industries are leading the charge:

- Semiconductors & Advanced Electronics – New chip fabrication plants are breaking ground across the Southwest, Midwest, and Southeast, representing billions in planned investment. These facilities have long construction timelines, but once operational, they anchor high-value industrial clusters.

- Energy Infrastructure – Rapid electrification and AI-driven data center growth are pushing the grid to expand. Investments in nuclear power, natural gas plant conversions, and LNG development are creating new demand for specialized manufacturing and support facilities.

- Aerospace & Defense – Rising geopolitical tensions are driving both domestic and international demand for aircraft, parts, and defense systems. Contracted manufacturing and supplier networks are scaling up to meet multi-year production goals.

- Specialized & Manufacturing Essential Assets (MEAs) – Industries like food processing, medical equipment, and infrastructure components tend to demonstrate steady, recession-resilient demand—qualities that can translate into stability for investors in related real estate.

The Commercial Real Estate Connection

Industrial and manufacturing properties often underpin long-term triple-net leases with tenants who have strong credit profiles. In growth hot spots, these assets can serve as anchors for entire ecosystems—supporting warehousing, logistics, and transportation infrastructure.

For example, in late 2024, U.S. industrial vacancy rates stood at 6.9%, below the long-term average, while rental rates continued to rise. Geographic clustering around manufacturing hubs tends to drive parallel demand in distribution and logistics real estate, creating a multiplier effect for industrial property owners.

How DSTs Can Help Expose These Opportunities for Your Clients

Accessing institutional-grade industrial manufacturing assets directly can be challenging for individual investors. This is where Delaware Statutory Trusts (DSTs) can bridge the gap.

As you know, DSTs:

- Meet IRS like-kind property requirements for 1031 exchanges, allowing clients to transition from active property management to passive ownership while deferring capital gains taxes.

- Are curated and vetted by experienced sponsors with deep due diligence processes—helping to identify viable manufacturing-oriented properties and tenants.

- Provide access to sectors historically reserved for institutional capital, including high-barrier-to-entry industrial manufacturing facilities.

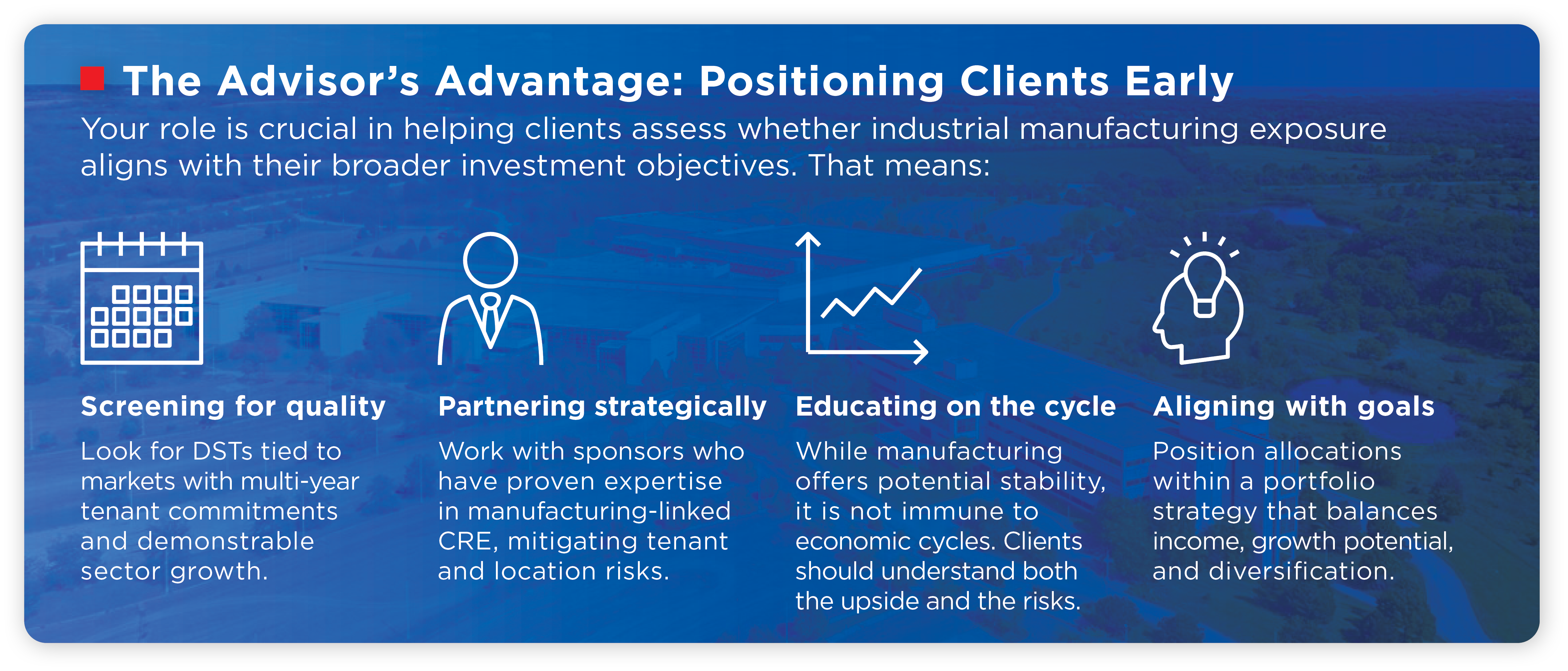

The Advisor’s Advantage: Positioning Clients Early

Your role is crucial in helping clients assess whether industrial manufacturing exposure aligns with their broader investment objectives. That means:

- Screening for quality – Look for DSTs tied to markets with multi-year tenant commitments and demonstrable sector growth.

- Partnering strategically – Work with sponsors who have proven expertise in manufacturing-linked CRE, mitigating tenant and location risks.

- Educating on the cycle – While manufacturing offers potential stability, it is not immune to economic cycles. Clients should understand both the upside and the risks.

- Aligning with goals – Position allocations within a portfolio strategy that balances income, growth potential, and diversification.

The U.S. manufacturing story is still unfolding, but the early signs suggest that certain sectors are already laying a foundation for long-term demand in industrial real estate. As an advisor, identifying these opportunities early and pairing them with the right DST structures could help your clients capture both stability and strategic growth potential.

Sources:

- U.S. Bureau of Economic Analysis, “Industry GDP Data,” 2025.

- Federal Reserve, “Industrial Production and Capacity Utilization,” June 2025.

- U.S. Department of Commerce, “CHIPS and Science Act Funding Summary,” 2024.

- U.S. Department of Energy, “Inflation Reduction Act: Clean Energy Investments,” 2024.

- Institute for Supply Management, “Manufacturing PMI,” July 2025.

- CBRE Research, “U.S. Industrial Real Estate Outlook,” Q4 2024.

Comments